Slättö House View

Slättö’s House View is our data-driven market deep dive, updated twice a year. We combine market data, stakeholder input, and internal discussions to form a clear base view of the Nordics and translate it into investment priorities - where to focus, where to be selective, and what to avoid.

Extensive analytical work sits behind the House View, and it helps us make better and faster decisions that support strong risk-adjusted returns for our investors.

This is backed by a strong deal flow. Over the last twelve months, Slättö has reviewed deals worth SEK 225 bn in asset value, corresponding to about 75% of total Nordic turnover, giving us unparallelled insights on pricing and liquidity.

Here is a summary of our latest market report. To access the complete report, please reach out to our team: ir@slatto.se.

Nordic Market Insights

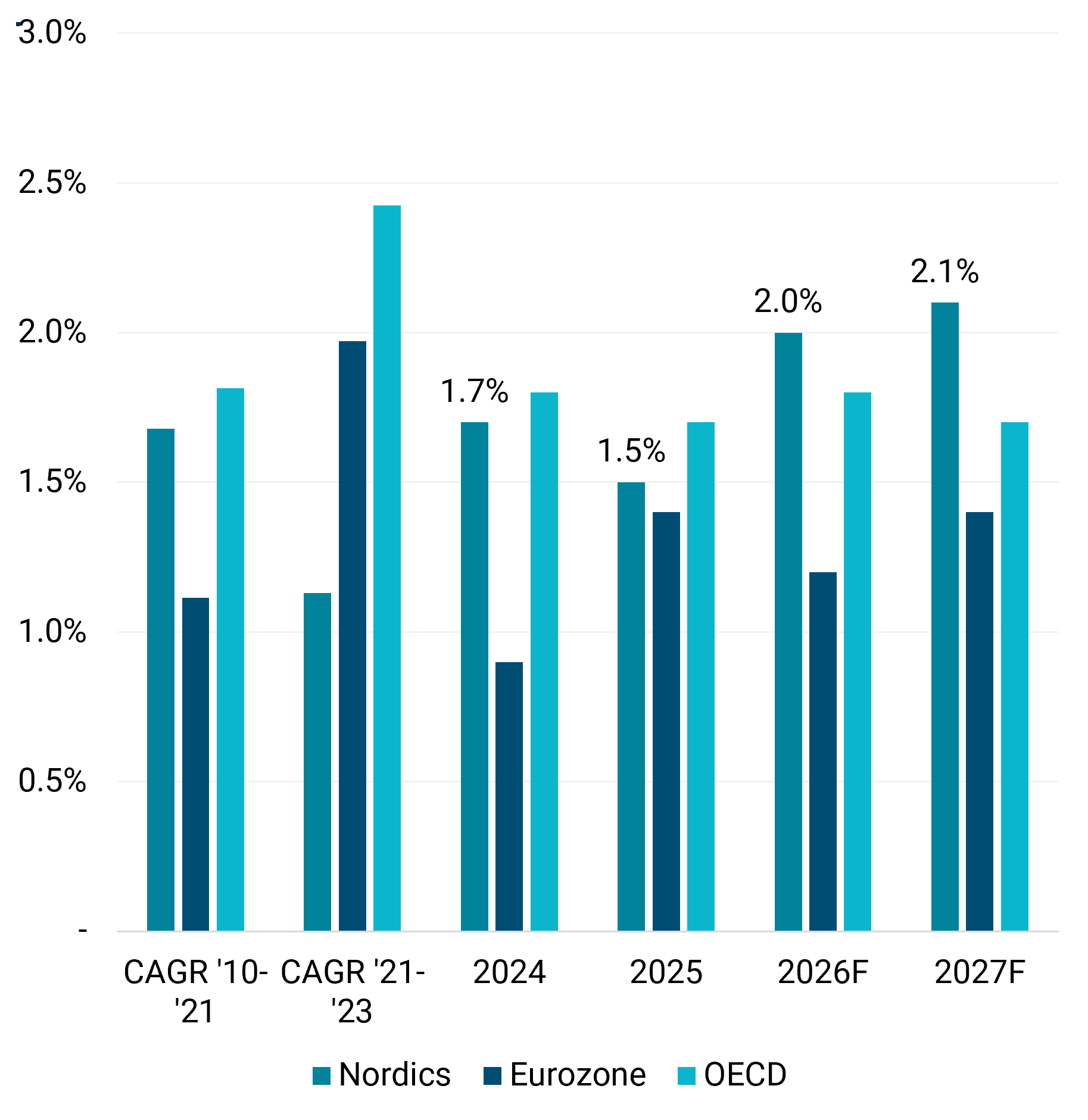

Nordic fundamentals remain strong with projected economic growth at 2%, in line with US and significantly ahead of the rest of Europe

Nordic GDP growth slowed to around 1.5% in 2025, largely due to weaker investment after the lagged effects of higher interest rates, but a recovery is expected from 2026 onward, with growth projected at ~2.0% per year in 2026 and 2027, which is in line with the United States and significantly ahead of Europe. The Nordic GDP growth is driven by Sweden and Denmark, while Norway and Finland are behind. Inflation is broadly normalising toward target levels into 2026 and 2027, and labour markets, while weaker since 2022, are expected to gradually improve.

However, the ongoing conflict in the Middle East introduces meaningful uncertainty into the economic outlook. Oil prices have risen sharply over the past week, with potential spillover effects on global inflation. A renewed inflationary episode could weigh on consumer spending, delay rate cuts, and dampen growth prospects globally.

That said, the Nordics are comparatively well-positioned to weather this turbulence. The region’s structurally low sovereign debt levels and triple A credit ratings underpin macro resilience and provide fiscal flexibility in downturns. In addition, the region scores high in global governance, ESG and innovation rankings providing a favorable backdrop for long-term growth.

- Nordic growth expected to outpace EU 2026-27.

- Nordic fiscal strength and governance support relative investment appeal in uncertain times.

SEB Nordic Outlook January 2026. Historical data from OECD

Excellent debt availability in the Nordics through stable banks and strong bond market

Credit sentiment indicators point to continued improvement in availability and Nordic banks remain stable and profitable and supportive of real estate credits. Importantly, banks are also being pushed to compete on pricing as mortgage growth stagnates and alternative funding channels reopen. The Nordic bond market has rebounded strongly after the 2022–23 dislocation and new issuance strongly recovered in 2024 and 2025 alongside tighter credit spreads. The bond market is open for both high yield and investment grade issuers. Sweden and Norway continue to rely on bank and bond financing structures, Finland is more balanced, while Denmark remains more tied to its domestic mortgage credit system.

- Strong bank and bond market sentiment.

- Bank’s are forced to compete on pricing as the bond market rebounds.

Swedbank

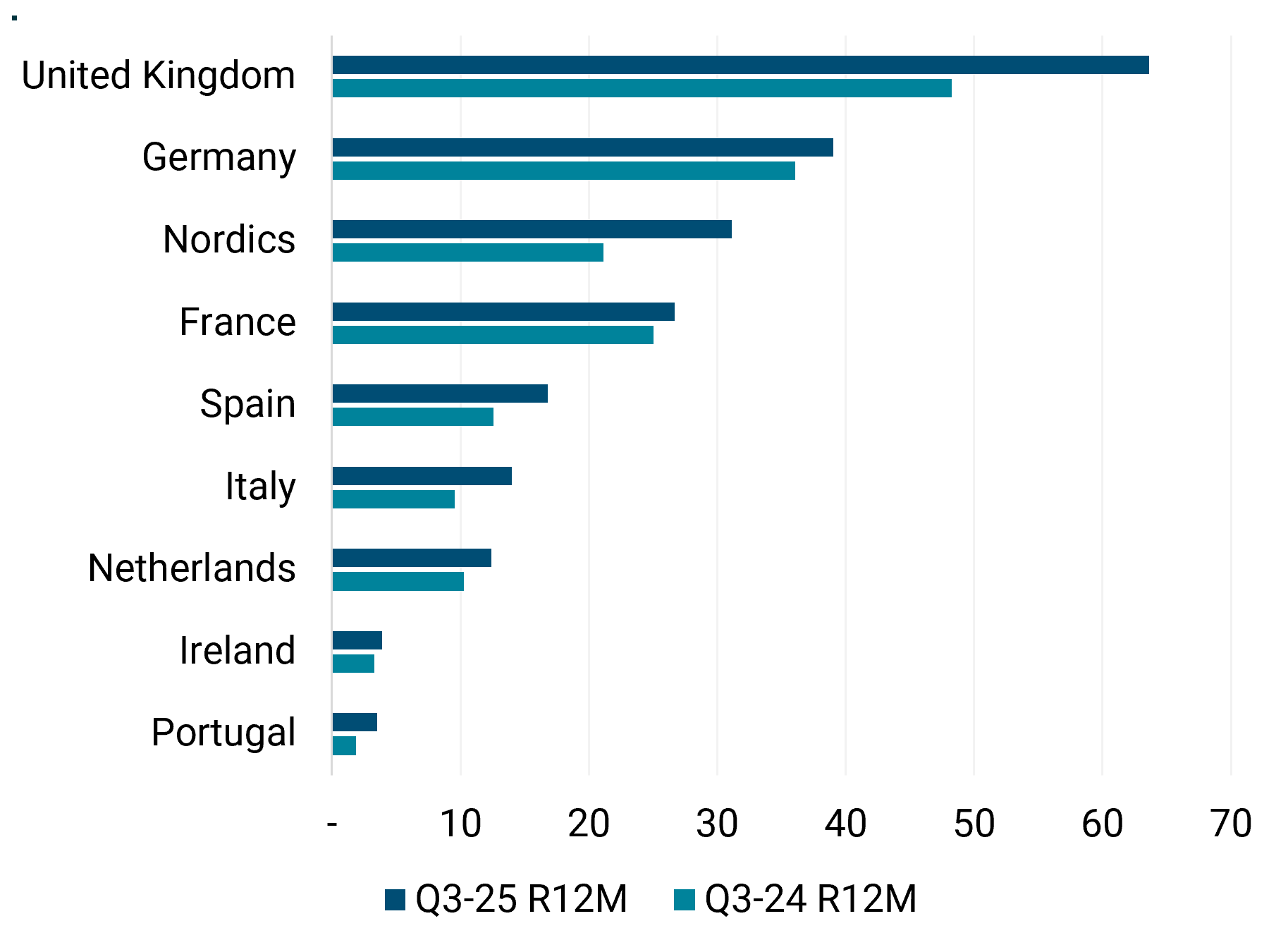

Nordic real estate investment market is the Europe’s third largest with liquidity improving

The Nordics remain one of Europe’s most liquid real estate markets and rank as the third largest market in Europe (after the UK and Germany) with high volume growth in 2024-25 compared to other major European markets. Transaction volumes are improving, but liquidity remains below pre-2022 levels; Sweden and Denmark are currently the most active and resilient markets, Finland is rebounding from a low base but structurally less liquid, and Norway shows a pause in momentum.

- The Nordics is one of the largest and most liquid markets in Europe.

- Liquidity is improving, led by Sweden and Denmark, but remains below pre 2022 levels.

C&W

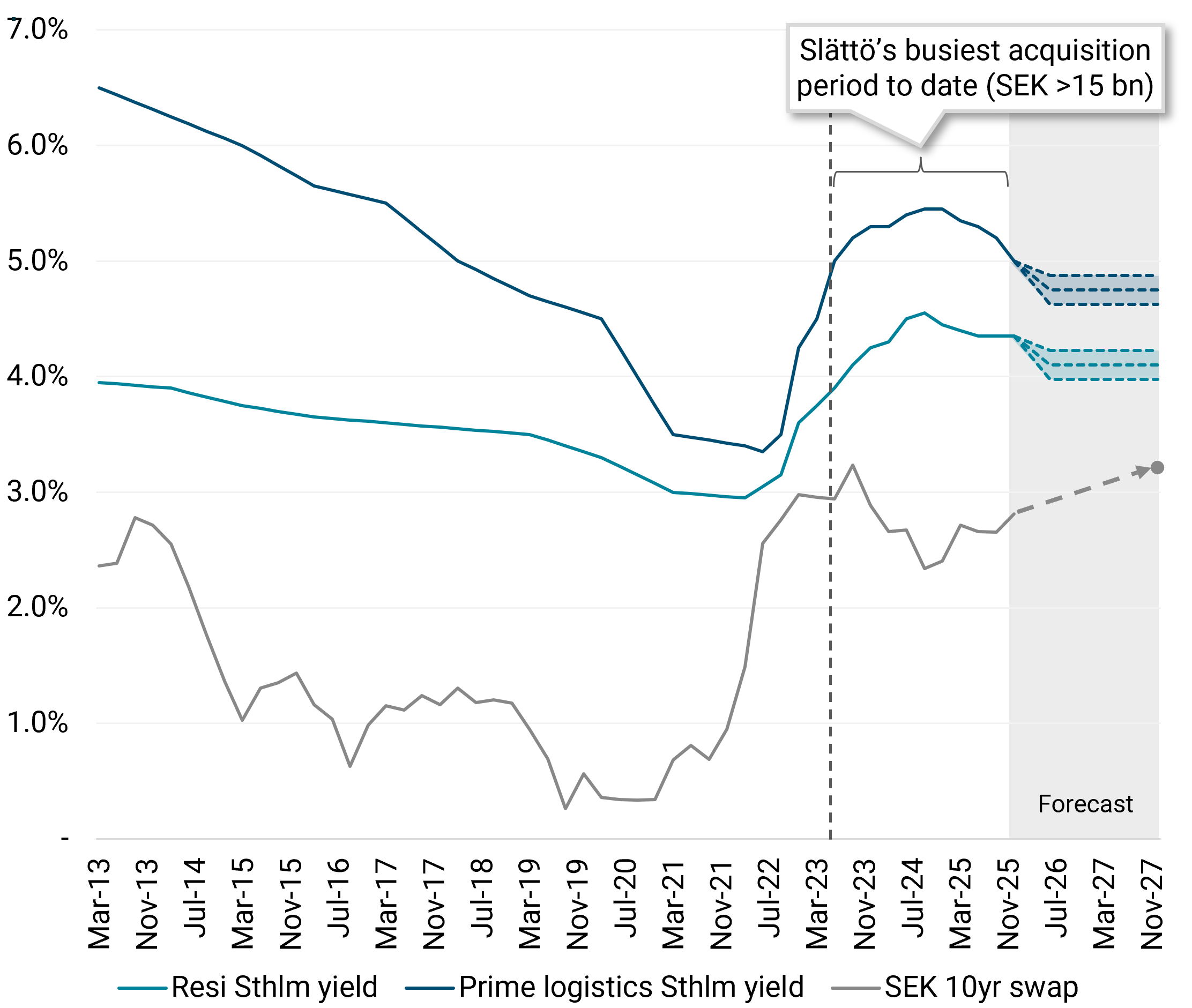

After one of Europe’s deepest repricing, yields are starting to compress in Nordic capitals

The Nordics rank among Europe’s most repriced markets, with larger peak-to-trough yield widening than most European peers. Importantly, unlike several European markets where yields still sit flat at peak levels, the Nordic capitals already show modest compression.

While the recovery has been tempered by global uncertainty, Slättö’s view is that the pricing trough is behind us and that further modest yield compression is likely over the next 12 months as liquidity improves. We expect the current attractive acquisition window to remain open into 2026.

- The Nordics rank among Europe’s most repriced markets.

- Slättö’s view is that modest yield compression is likely over the next 12 months as liquidity improves.

Yield data from Newsec and Swap data from Capital IQ. Slättö forecast

Swedish listed Real Estate market is a key source of equity and driver of liquidity

The main Nordic stock exchanges host 45 real estate companies, of which 40 on Nasdaq Stockholm. The combined market capitalisation amounts to around EUR 60 bn. Over the last years, the real estate index has underperformed versus broader indices amid rising interest rates and property yields as well as operational concerns. The sector trades at around 30% discount to net asset value, but the difference between companies is wide. The valuation spread in terms of price in relation to net asset value is wider than price in relation to cash flow measures. Public market investors favor high yielding property companies with logistics and light industrial being the only segment trading at a premium to net asset value.

- Public real estate market still trades at discount.

- Investors favor high yielding companies.